“Why does a one-month supply of insulin cost over $1,000.00 in the USA whereas a six-month supply of the very same insulin, produced by the same Big-Pharma manufacturer, cost less than $100.00 in Tijuana, Mexico? Shouldn’t a product like insulin cost the same all around the world- or at least be priced in the same unit of account, like Bitcoin, which is really nothing more than the time value of energy? Remember: one bitcoin is equal to one bitcoin, a currency for one world and one race- the human race.”

-Alexander J. Singleton

“In the long-run we are all dead; it is the short run that counts- but the question is how long will the short-run last?” asked Ludwig Von Mises within the preface of his seminal Theory of Sound Money and Credit; he bluntly answers his own question by blaming statesman and politicians considerably overrating the duration of the economic short-run, which we now appear to be outliving- a diagnosis all too familiar for another round of “quantitative easing” to delay the inevitable fiscal and monetary woes in the wake of the Great Recession (Mises, L. V., & French, D. E.). As of April 2008, the housing-crisis had been quarantined as “subprime contagion,” comprising only about 20.6% of the housing-market ($1.4 trillion); however, like a brewing economic storm, all of the aforementioned elements had yet to be realized, as the housing-crisis erased nearly $19.2 trillion dollars in wealth (2011 dollars) and a loss of 8.8 million jobs, while many millions more became underemployed- all apparently acceptable collateral-damage in addition to another tragic social-cost of central-banking: a growing opioid epidemic. Sporadic gentrification throughout the southeast disturbingly coincided with the onslaught of the opioid epidemic, ultimately surging throughout the early 2000s and peaking in 2015 as noted by President Obama that more Americans now die from drug overdoses than they do from motor vehicle crashes: back in 1999 there were more than twice as many fatalities associated with motor vehicle accidents vs drug overdoses; by 2014, there were 29,230 motor vehicle deaths and 47,055 individuals dying due to fatal drug overdoses (American Opioid Addiction Epidemic. (2017, August 18)).

As the labor force participation rate in the United States peaked at 67.3% in early 2000, it has declined at a more or less continuous pace ever since, reaching a near 40-year low of 62.4% in September 2015– all measures conveniently sanitized every quarter by the Department of Labor (Krueger, A. B. (2017). Nearly a decade later, in addition to a massive Treasury Asset Resolution Protection (TARP) bailout totaling over $2.3 trillion dollars, the Dow Jones Industrial Average is off roughly 9.3% from an all-time high of 26,616- crisis averted? How much has this “recovery” really cost to service the quantitative-easing cure-all, which is basically Fed-Speak for monetizing debt via expansion of the money-supply (The Financial Crisis Response In Charts(Rep.)? The sobering reality is that the real-rate of annualized inflation over the course of the last decade has been approximately 7% per year, while Consumer Prices have soared 160% since 2001, which is exactly why the capital-class typically demands at least a 7% return on investment by any legitimate wealth-manager (Revealing The Real Rate Of Inflation Would Crash The System. (n.d.). Look no further than a grocery-store aisle- a 20 ounce box of Kellogg’s Raisin Bran costed about $1.99/20 ounce box back in 2006- or $0.09 per ounce; in 2019, a 13 oz box of Raisin Bran costs $5.29 for a 13 ounce box, $0.40 per ounce- a 400% increase in price over the last decade (OccupyWisdom).

America has a deficit of trust. As Fed Chair Greenspan once said, inflation is the hidden confiscation of wealth- so indeed, as Von Mises put it, it is the opium of the people administered to them by anti-capitalist governments and parties (Mises, L. V., & French, D. E.). According to Friedrich Hayek, contemporary politics is based on the assumption that government has the right to create and make people accept any amount of additional money it wishes, and so for that same very reason, it will reserve the right; however, Hayek argues a government not ought to be able to take whatever it wants, but be limited strictly to the user of the means placed at its disposal by the representatives of the people and, and to be unable to extend its resources beyond what the people have agreed to let it have, which is not worth overextending beyond finance, infrastructure and education for Wealth of Nations- as argued by Adam Smith (Denationalisation of Money the Argument Redefined). Is government the best custodian of fiscal and monetary policy? Is a truly free-market more responsible than a crony-capitalist, “Revolving-Door” type of government? Are commerce and trade even possible without government? In 1988, cryptographer Timothy C. May, stated “Crypto-anarchy will alter completely the nature of government regulation, the ability to tax and control economic interactions, the ability to keep information secret, and will even alter the nature of trust and reputation.” Indeed a peer-to-peer electronic cash system without relying on trust in a centralized-authority may be the strong-medicine required in lieu of the QE-withdrawals in order to rebalance a deficit of trust- known today as Bitcoin. In 2009, within an obscure corner of the internet, an anonymous person or persons published a math paper — the “Bitcoin white paper” — solved a problem that had until then stumped computer scientists: how to create digital money without any trusted parties; the key breakthrough was the invention of a cryptographic data model called a blockchain: recall that, at the time, the financial system was experiencing a run on the banking system- the credit crunch was made worse by a lack of clarity around asset ownership (Ludwin, A. (2016, June 06)). The crisis, and its causes, were not lost on the author of this paper; in fact, he or she cited the financial crisis directly by embedding a link to a Times of London article about bank bailouts in the first Bitcoin transaction (Ludwin, A. (2016, June 06)). Originally conceived by Satoshi Nakamoto one decade ago this coming October, Bitcoin is gradually gaining widespread adoption “understood as distributed software that allows for transfer of value using a currency protected from unexpected inflation without relying on trusted third parties;” in other words, Bitcoin automates the functions of a modern central bank and makes them predictable and virtually immutable by programming them into code decentralized among thousands of network members, none of whom can alter the code without the consent of the rest (Ammous, S. (2018)). Scholar, statistician, former trader, and risk analyst, Nassim Nicholas Taleb, likens Bitcoin as the world’s first organic currency as its mere existence is an insurance policy that will remind governments that the last object the establishment could control- currency is no longer their monopoly (Ammous, S. (2018)). A Healthcoin could give us an insurance-policy against an Orwellian future- for not only the future of money but healthcare as well: the future of Bitcoin may merge with Ethereum SmartContracts as a Blockchain for the greater good of humanity. (Ammous, S. (2018)).

Cryptocurrency began long before Bitcoin and Ethereum, even before eGold and HashCash- perhaps as far back as the early 80s or late 70s in the arcades. Borrowing once again from Timothy C. May but this time from his “Untraceable Digital Cash, Information, Markets, and Blacknet” concept as “Anyone a Mint,” he suggests that anyone can essentially become a mint of digital-cash if and when the “customer-shop-mint” relationship is bypassed: meaning that an open-source, decentralized infrastructure could verify and authenticate transactions between individuals or entities without relying on a centralized, third-party authority- people could conceivably create their own cash, or currency, but it must be backed by something or store value. According to Peter Schiff’s Crash Proof, currency must satisfy the following requirements:

- A unit of account

- A store of value.

- Medium of exchange.

- Method of Deferred Payment.

Data is the new oil: it is extracted, collected, refined, studied and, and most of the time, sold without the users-consent- from social-networks like Facebook to electronic medical record companies like Cerner. One of the easiest ways to think about someone creating their own currency is to envision their health-behaviors as a tokenized asset, or store of value- in the not too distant future, individuals may have the ability to record their exercise activity, nutritional intake or vital-stats taken during a healthcare visit, which would value the “fitness” of their token.

Ask a doctor or surgeon how much a procedure will cost- if prescriptions are involved, ask the pharmacist how much the drug actually costs and why insurance is required in order to benefit from discount pricing. Why does a one-month supply of insulin cost over $1,000.00 in the USA whereas a six-month supply of the very same insulin, produced by the same BigPharma manufacturer, cost less than $100.00 in Tijuana, Mexico (Prasad, Rita)?

Shouldn’t a product like insulin cost the same all around the world- or at least be priced in the same unit of account, like Bitcoin, which is really nothing more than the time value of energy? Remember: one bitcoin is equal to one bitcoin, a currency for one world and one race- the human race.

Health-insurance is now nothing more than a glorified payment-processing system that is unfairly inflated by reckless Medicaid and Medicare government-spending. According to the Economist, the estimated total of healthcare fraud in 2011 was $272 billion dollars- or approximately 10% of total healthcare spending in America amounting to $2.7 trillion dollars, accounting for 17% of overall American GDP; American healthcare spending alone would be the fifth largest country in the world by GDP (The $272 Billion Swindle). The World Health Organization estimates counterfeit pharmaceuticals cost over $200 billion dollars in lost revenue in 2017 and lead to more than 1 million deaths every year (Finan, Terence). Transactions validated on an open-source, cryptocurrency ledger could potentially prevent a total estimated $2.68 trillion in fraud committed per year in the global public-sector, world-wide pharmaceutical industry, US healthcare and banking systems. How can a healthcare system fraught with so much fraud sustain itself without any fiscal discipline or accountability? A unit of account is essential for all forms of economic calculation and planning, and unsound accounting makes economic calculation unreliable and is the root cause of economic recessions and crises (Ammous, S. (2018)). Financial accounting is not only the language of business and production but the “spreadsheet of civilization” as consumers demand the quantity and quality of goods and services produced; so it is the consumer who determines profit and loss for a given company, if and only if, it is accountable- financial accounting forces producers to obey the consumer, communicating whether or not a business is satisfying customers: if a business is successful, it is profitable, and if it is failing, it reports a loss (Mises.org: Socialized Medicine: An Accounting Perspective). However, accounting is impossible without prices to record or if the ledger is tampered, altered or otherwise immutable and also a reason why socialized medicine is theoretically impossible- because buyers do not pay money in exchange for goods or services (Mises.org: Socialized Medicine: An Accounting Perspective).

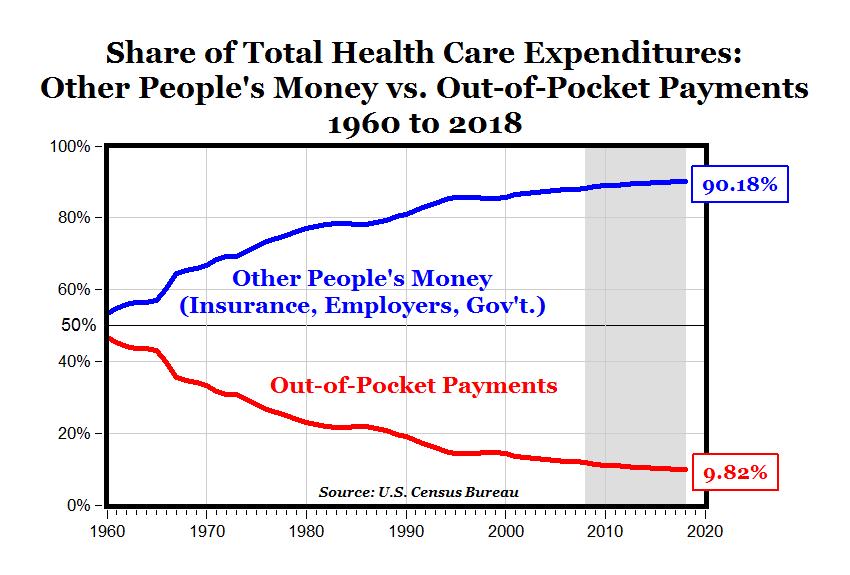

Beginning in the 1940s, government policies distorted the healthcare market, causing prices to rise and denying many Americans access to quality care, with out-of-pocket expenses originally representing 47.6% of expenses in 1960 just 10.5% of out of pocket payments: a moral-hazard has been replaced with a socialized healthcare stop-gap- but at what cost? (Ron Paul Warns “Middle Of The Road In Healthcare Leads To Socialism,” (n.d.)). Without individual accountability there is no personal responsibility to maintain health, which is why 1 in 3 Americans are obese at the expense of the fit; since the 1950s, seven Presidents have tried but failed to repeal the US healthcare system- only a practical solution like a “healthcoin” as a health-insurance cryptocurrency alternative would have any chance of sensibly replacing the $3.2 Trillion US Healthcare system – THAT AGAIN – WOULD BE THE 5TH LARGEST ECONOMY IN THE WORLD if it were its own separate country, according to World Bank (Butler, S. M. (2017, February 01)).

Imagine people betting on their health and fitness on a decentralized exchange like Augur Project or DAOcasino, writing or selling covered call-options from an Ethereum token in an attempt to generate income-payable from their very own ERC20 token instead of paying never-ending monthly health-insurance premiums that only seem to increase along with higher-deductibles. Adapting optionality for health-insurance coverage, and portfolios for health-care providers, suppose a new type of health-insurance was reinvented as self-assembling pools of individuals categorized according to healthy behaviors and risk-profiles with verifiable data recorded on a cryptocurrency token or smart-contract layer, anonymously but publicly traded on an exchange: healthcare-options could be derived from tokenized-data and priced by algorithmic health-insurance brokers and artificially-intelligent traders, whereby individuals could exercise the right to strike optional health-coverage during terms and conditions specified in the options-contract- after all, health is always subject to change sooner rather than later. Healthcare price-discovery could be optimized with an options-contract instead of traditional health-insurance coverage with anonymized personal health-care data priced on a truly open market by combining Ethereum Smart-Contracts and ERC20 tokens with Hyperledger Burrow.

“Optional” Healthcare Insurance

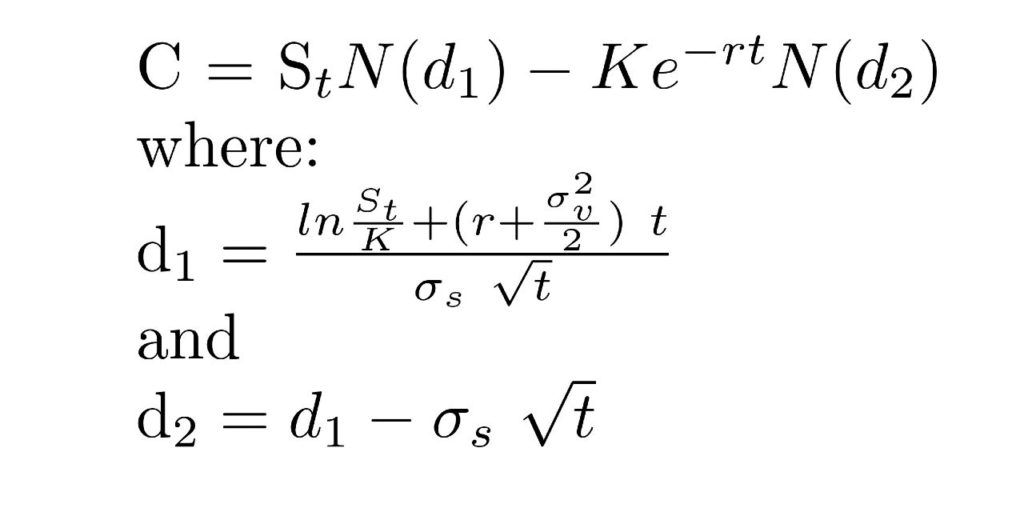

According to Nassim Taleb, “if you ‘have optionality,’ you don’t have much need for what is commonly called “intelligence,” “knowledge,” “insight,” “skills” and these complicated things that take place in our brain cells- for you don’t have to be right that often: all you need is the wisdom to not do unintelligent things to hurt yourself (some acts of omission) and recognize favorable outcomes when they occur; (The key is that your assessment doesn’t need to be made beforehand, only after the outcome),” (A Dozen Things I’ve Learned from Nassim Taleb about Optionality/Investing)- optionality and taking small bets (with preferably unlimited upside and limited downside) is the best route to prepare yourself for the random events that await you: in preparing for volatility in this manner, you give yourself the chance to not only withstand but to succeed and prosper in a big way (Elyassi-Rad, N. (2016, September 22)). Financial options are contracts between buyers and sellers that give buyers the right, but not the obligation, to buy (a call option) or sell (a put option) the underlying asset at a later date for a predetermined price- should the market not be favorable to the buyers’ “bets,” buyers may decide to let the option expire, that is, not to exercise it; in 1973, Black and Scholes derived a differential equation that must be satisfied by the price of any derivative dependent on a non-dividend paying stock- the Black-Scholes model is a rapid way of calculating the value of a European option (call option denoted below)(Chicaíza, L., & Cabedo, D. (June 2009)) (See Figure 7):

- N(•) is the standard normal cumulative distribution function.

- T – t is time to maturity.

- S is the spot price of the underlying asset.

- K is the strike price.

- r is the risk-free rate (annual rate, expressed in terms of continuous compounding).

- σ is the volatility in the log – returns of the underlying.

As simple as it is in this form, the model depends on very strict assumptions (Hull 2008):

- The stock price follows a geometric Brownian motion with μ and σ constant.

- The short selling of securities with full use of proceeds is permitted.

- There are no transaction costs or taxes.

- All securities are perfectly divisible.

- There are no dividends during the life of the derivative.

- There are no riskless arbitrage opportunities.

- Security trading is continuous.

- The risk-free rate of interest, r, is constant and the same for all maturities.

For the intents and purposes of a proposed “healthcoin” prototype, it is important to focus on two specific variables of option pricing: time to expiration and volatility; when either of these two variables increases, the value of the option (call or put) increases as well – both variables are key elements defining uncertainty, which is typically considered as a negative element in investment decision making (Hull 2008) (Chicaíza, L., & Cabedo, D. (June 2009)). Maintaining the definition previously provided for financial options, a real option is similar but applied to a real, tangible, or intangible asset, rather than a financial underlying asset: a real option is the right, but not the obligation to undertake a business decision (Chicaíza, L., & Cabedo, D. (June 2009). Since an option is merely a form of insurance or “hedge,” alternative concepts were first presented by Stew Myers (1977) when he posited that some corporate assets, especially growth opportunities, could be viewed as call-options: some investment opportunities grant the right, but not the obligation, to take specific operating action in the future or as Bowman and Hurry (1993, p. 761) explained it: “despite the of formal option contracts, they allow a similar pattern of investment behavior to occur,” (Chicaíza, L., & Cabedo, D. (June 2009)):

Concordantly, “real options represent choices (strategic or tactical) under conditions of risk and uncertainty about tangible and intangible (knowledge-based) assets (as compared and contrasted to financial assets) that encompass timing, selection and sequencing attributes of significance for the entity that may choose to exercise those options or not (individual, society or company);” an option isn’t merely a financial instrument insofar as it can be applied to insuring-risk against healthy decision-making or behavior (Carayannis, E. G. & Sipp, C. M., (2013)). Option valuation differs from the valuation of other assets in that risk and uncertainty are key factors: both volatility and time to expiration greatly impact the value of an option- it is how uncertainty is captured and included in the valuation model that has since then interested managers translating options into the physical world lead to the development of real options (Carayannis, E. G. & Sipp, C. M., (2013)). One of the lines of research referred to in the proceeding section is the relationship between option contracts and health-insurance operations; however, the financial options-markets created in the nineties constitute an alternative to the traditional coverage method- the reason is probably very simple: options-contracts and insurance and reinsurance operations are conceptually very close to each other as noted from the Chicaíza, L., & Cabedo study (Chicaíza, L., & Cabedo, D. (June 2009)):

- Both are hedging operations: options cover agents against unexpected changes in prices, while insurance covers agents against unexpected contingencies (accidents, illness, etc.).

- A premium must be paid: for both options and insurance contracts a premium must be paid. The buyer (options) / insurance (insurance) must pay a premium to the writer (options) / insurer (insurance) in order to obtain the desired hedge.

- Compensation: when an unexpected situation arises, compensation must be paid. If, for example, an accident occurs, the insured will receive compensation. If an unexpected change, the buyer will execute the option and receive an amount (compensation) equivalent to the difference between the strike price and the market price. In any case, if the unexpected situation does not arise, both the insured and the buyer lose the premium paid.

- Hedge period: timing of both insurance and option operations is relatively short. Despite the fact that the time horizon of insurance can be set in years, it is always possible to unilaterally withdraw from the contract; the insurance company may be required to increase the premium, or demand that the agent objectively is not able to fulfill. Alternatively, the agent may decide to pay the premium and thus withdraw from the insurance contract. Similarly, options may be established for long periods, but options are seldom entered into a financial year.

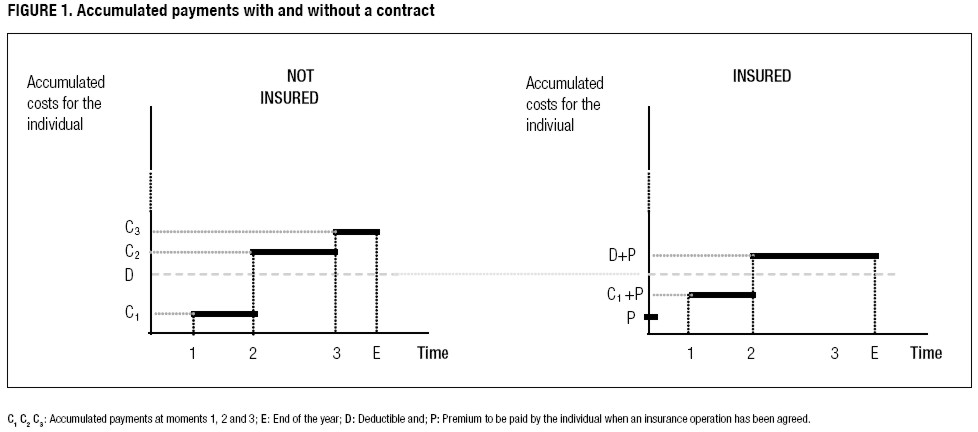

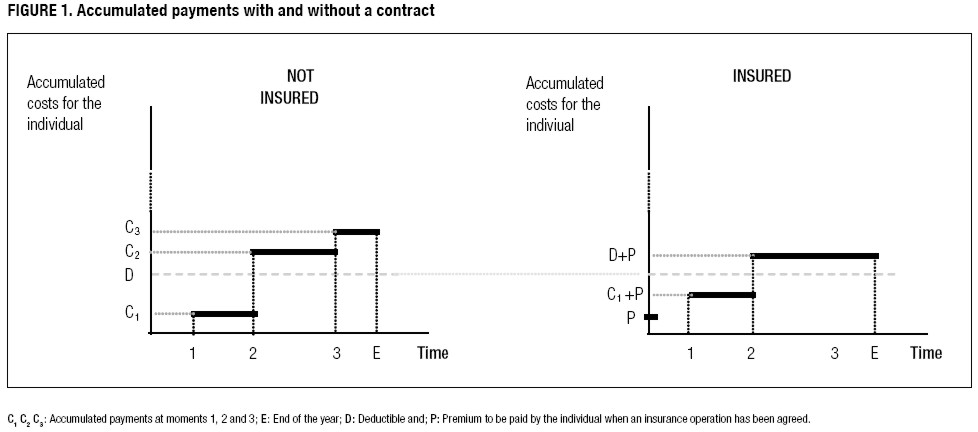

The Chicaíza & Cabedo studies outlined two scenarios for a given use-case of a covered-call option mitigating health cost risk in lieu of conventional health-insurance; in the first figure, the scenario on the left suggests that the incremental change in cost of healthcare is inversely proportional to any insurance coverage whatsoever, whereas the second scenario on right in the below figure outlines the accumulated costs of individual healthcare cost mitigated by insurance (Chicaíza, L., & Cabedo, D. (June 2009)).

Obviously, with health-insurance there is a maximum cost incurred by the individual (as depicted by the right side of the figure)- or “in nominal terms, the total cost will be deductible plus the cost of the premium paid to the insurer at the beginning of the year; if the risk has not been insured, the individual must assume the total cost of treatment, which, in the situation represented in Figure 1 is higher than the cost when it is insured” (Chicaíza, L., & Cabedo, D. (June 2009)).

{kind=link}

Independent Study

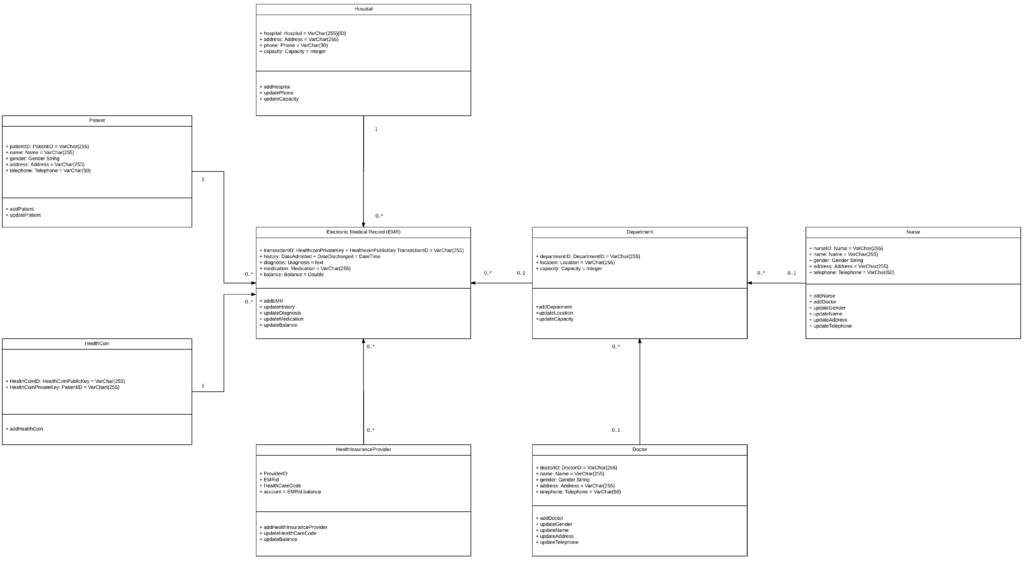

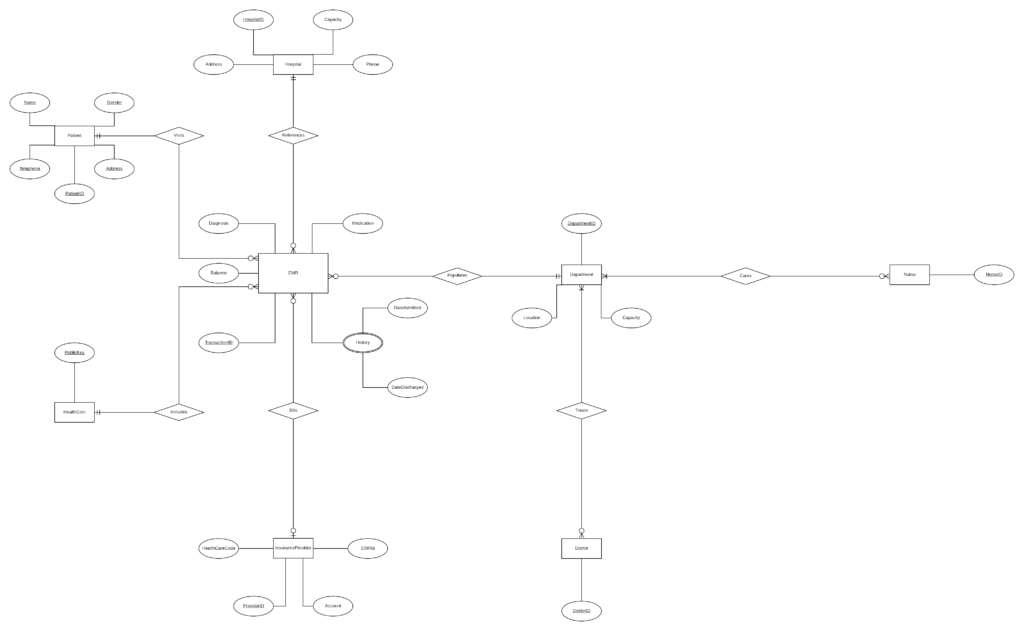

Conceptually, Ethereum Smart-Contracts can be understood as stored procedures that are associated with specific transaction records (for example, a value transfer in the Bitcoin stack cannot be completed without executing a short program written in Bitcoin script)- unlike a stored procedure in a centralized system, smart-contracts are executed by all nodes in the peer-to-peer network, resulting in challenges in scalability, manageability and funding of resource consumption (Valdes, Ray, et al.). A HealthCoin-Blockchain-based protocol for electronic medical records integrating additional attributes with the Bitcoin Script programming language or top of a second layer like the Ethereum ERC20 platform could conceivably store patient-data into one consolidated distributed electronic medical record (EMR), or anonymized ledger of contracts, instead of scattering multiple electronic medical-records between facilities and visits. In the case of HealthCoin, a patient could create a digital-wallet with a self-issued, unique private and public-keys specified according to the parameters assigned by the HealthCoin blockchain-protocol- so the patient’s digital-wallet private-key effectively becomes a universal patient-ID corresponding to a public-key anonymously interacting with the HealthCoin blockchain-network. The composite-key relationship defined by the patient-private key and the HealthCoin public-key defines the unique-EMR session-ID for a given health-care visit, creating a new EMR-record, or EMRID. Upon instantiation, health-care professionals could effectively AND efficiently retrieve patient vitals and other data, such as recent physical-activity, diet or recent healthcare visits, thereby enabling doctors and nurses to focus on the patient instead of paperwork. Hospital administrators typically organize departments of doctors and nurses operating as units who treat according to the data reported on the patient-chart before interacting with the patient. Upon finishing treatment, but before hospital-discharge, the patient EMRID session is closed and their data is given back to their HealthCoin digital-wallet via QR-code- because after all, it is data that belongs to a patient, not a corporation or government.

CIOs and executives who haven’t initiated blockchain are often worried about “missing out” and desperately want to pilot projects. Healthcare industry sectors are poised to capture tremendous blockchain ecosystem potential- specifically for healthcare payers and providers, blockchain promises to bring new ways of managing how the industry transacts business and exchanges information (Shanler, Michael, et al.). Healthcare provider credentialing, medical records exchange, medical billing and claims management are just a handful of examples of blockchain projects that have high potential and for life science, blockchain holds clear potential for anti-counterfeiting, e-pedigree, contracts, health records and clinical trial documentation; the Gartner thinktank anticipates the following benchmarks within the next several years (Shanler, Michael, et al.):

- By 2020, 20% of both major healthcare payer and provider organizations will pilot initial use cases for blockchain in healthcare settings.

- By 2021, 25% of blockchain pilots and proofs of concept across life science organizations will be applied to anti-counterfeiting.

- By 2020, 80% of life science blockchain projects started before 2016 will have failed to move into production.

McKinsey found 64 different use cases for blockchains in a survey of 200 companies. The report claims that the insurance industry has the largest non-bitcoin blockchain solutions, with 22 percent, followed by the payments industry, with 13 percent- financial Services in general make up 50 percent of the total mix (Parker, Luke). In terms of dollars value, the biggest revenue generating sector is cross-border business to business payments, generating between $50-$60 billion, followed by trade finance with $14-$17 billion (Parker, Luke). McKinsey also conducted a study examining 24 use cases focused on financial services applications: seven of the subject applications studied were referred to as “genuine use cases” that addressed “associated pain points” with today’s systems, indicating that they will generate the most revenue and be the most pursued- between those aforementioned seven use cases, McKinsey is expecting Blockchain to “generate ~$80B to 110B in impact (Parker, Luke).”

- Trade Finance, where it can lower costs and speed up turnarounds to a revenue boost of between $14 and $17 billion.

- Cross-border B2B payments, where lower costs and fees plus speedier delivery will save them around $50 – $60 billion.

- Cross-border P2P payments, which like B2B payments can lower costs while adding speed, but do so for personal remittances, should add $3 – $5 billion to their bottom line.

- Repurchase Agreement Transactions, where blockchains will lower operational costs and systematic risks, is worth around $2 to $5 billion.

- Over The Counter Derivatives, where streamlined settlements lead to reduced operational costs and need for capital. $4 – $7 billion more saved here.

- Know Your Customer / Anti Money Laundering Management, because it reduces duplicated effort and smooths the on-boarding process, worth between $4 and $8 billion.

- Identity Fraud, where more security leads to fewer damage payouts and happier customers. $7 to $9 billion saved here as well.

Noting that the Venture Capital investments for blockchain startups are now coming off their early 2015 highs, the report points out that the established banking industry is pouring money into blockchain technology far faster and more steadily, and a likely target of $400 million during 2019 (Parker, Luke.).

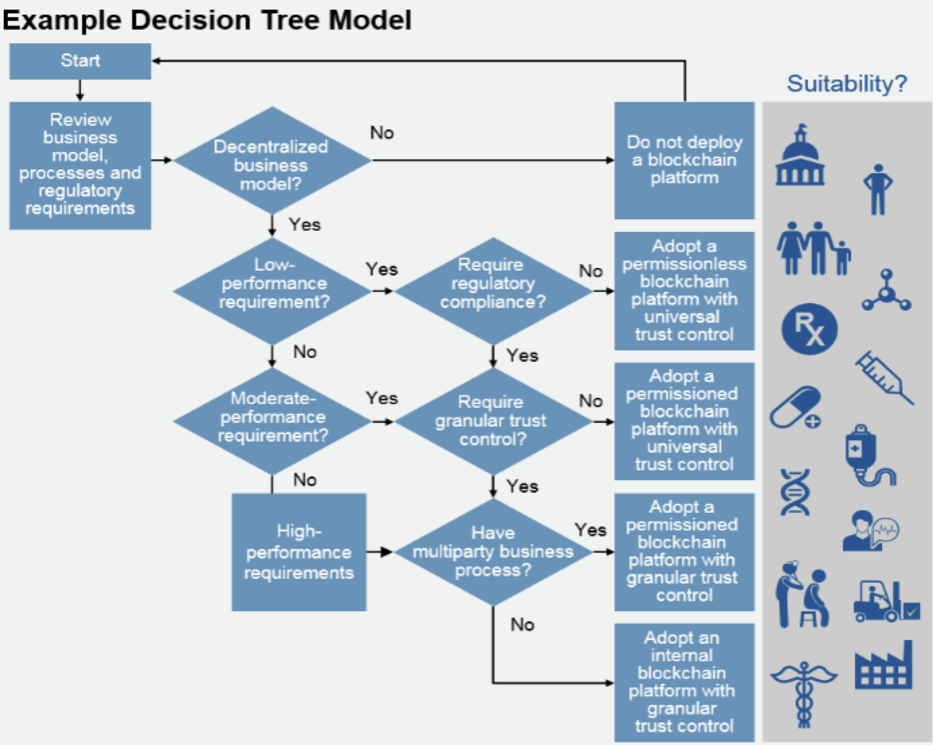

Only 1% of responding CIOs indicate any kind of blockchain adoption, and only 8% of CIOs are in short-term planning and pilot execution. Seventy-seven percent of responding CIOs say their enterprise has no interest in the technology and/or no action planned to investigate or develop it (Furlonger, David, and Rajesh Kandaswamy.). Gartner has estimated that by 2022, so-called ratified unbundled (i.e. defined impact) smart contracts will be in use by more than 25% of global organizations (Panetta, Kasey). Consider these scenarios that illustrate distinct options for decentralization and establishing trust (Shanler, Michael, et al.):

- A large-scale genomic bank, in which millions of patients and consumers can share their genomic information with drug companies running R&D, may be able to coax participation using a public decentralization approach. A permissionless platform will mandate that a network of consumers with different diseases, biomarkers and treatments establish trust with one another.

- A blockchain-based health system that expands across a series of payer and provider networks may gravitate toward more of a consortium-based decentralization model. Here, a permissioned blockchain platform, where trust is shared across the different major players, may be the best fit.

- A serialization and anti-counterfeiting effort by a drug company would require more of an internal blockchain platform, in which the sponsoring entity establishes compliance, validation and control.

- Provider directory and credentialing decentralize certification and verification efforts, while allowing payers and providers to access or update information without duplicated efforts.

According to Accenture research published at the start of 2017, investment banks alone could save up to $12 billion per year by adopting blockchain and smart contracts, effectively a program code that automatically performs some actions when predefined conditions occur (i.e. if X does Y, then execute Z)- just this year, blockchain start-ups amassed more than $3.25 billion in funding through token sales (Aitken, Roger). Cutting out middleman means savings for the business: according to a McKinsey report, it is estimated that blockchain could save businesses at least $50 billion in B2B transactions by 2021 (Aitken, Roger). Per Gartner, by 2020, the banking industry will derive $1 billion in business value from the use of blockchain-based cryptocurrencies; by 2018 YE, at least one Tier-1 bank will offer crypto services (including some form of “counterparty” services to insure expected value) and by year-end 2019, at least one Tier-1 bank will include cryptocurrencies in its asset portfolio (Kandaswamy, Rajesh, et al).

Collectively, financial services and insurance firms are in the vanguard of planning and experimentation activity; transportation, telecom, government and utilities sectors are now becoming more engaged- this is likely due to the heavy focus on process efficiency, supply chain and logistics opportunities (Furlonger, David, and Rajesh Kandaswamy). For telecom, the interest is in a desire to “own the infrastructure wires” and grasp the consumer payment opportunity (Furlonger, David, and Rajesh Kandaswamy).

Scalability means many different things to different businesses. Gartner defines scalability as “the measure of a system’s ability to increase or decrease in performance and cost in response to changes in application and system processing demands;” examples would include how well a hardware system performs when the number of users is increased, how well a database withstands growing numbers of queries, or how well an operating system performs on different classes of hardware because enterprises that are growing rapidly should pay special attention to scalability when evaluating hardware and software,” (Litan, Avivah, and William Clark). Behavioral incentives are an emerging trend within healthcare, already offering a promising value-proposition ahead of tokenized blockchains. A recent study conducted by Harvard University examined a program that offered financial incentives to both patients and their physicians to control low-density lipoproteins (LDL) cholesterol may be a cost-effective intervention for patients at high risk of cardiovascular disease (CVD), according to new research led by Harvard T.H. Chan School of Public Health; the study revealed that the shared incentive program provided significant value offer improved outcomes even when accounting for additional costs, such as electronic pill bottles to monitor drug adherence, more frequent cholesterol measurements, administrative expenses, and the actual cash incentive, which maxed out at $1,024 per year, split between the doctor and patient (Sweeney, Chris). Personal blockchains tokenizing healthy behavior may prove to be far more fairly efficient than current practices today.

What is a token and how does it differ from a blockchain? All blockchain-based cryptocurrency coins (e.g. Bitcoin, Ethereum, Litecoin etc) are tokens, but not all tokens are blockchain-based coins. Coins (that are also often called altcoins or alternative cryptocurrency coins) are digital money, created using encryption techniques, that store value over time- a digital equivalent of money; Bitcoin is the most famous example based on blockchain — public and distributed digital ledger, where all transactions can be seen. Data is stored collectively and shared between participants of blockchain network (What Is the Difference Between Coins and Tokens?). A cryptocurrency-coin generally exhibits the following characteristics (What Is the Difference Between Coins and Tokens?):

- Cryptocurrency-coins have the same characteristics as money: they are fungible, divisible, acceptable, portable, durable and have limited supply.

- Cryptocurrency-coins are tied to public-open blockchain — anyone is allowed to join and participate in the network.

- Cryptocurrency-coins may be sent, received or mined.

- Cryptocurrency-coins are not meant to perform any functions beyond money.

Again, all blockchain-based cryptocurrencies (e.g. Bitcoin, Ethereum, Litecoin etc) are tokens, but not all tokens (e.g. ERC20 and ERC 721) are blockchain-based cryptocurrencies. Tokenization, the process of creating a token, is not blockchain dependent; while blockchain technology drives some of the transformation of tokenization constructs, other types of tokens (such as industry protocols) are essential to digital ecosystem expansion (Uzureau, Christopher, et al):

- In its fundamental form, a token is a representation of value, assets, identity or information, as well as an output of the contractual agreements defined by the underlying company/institution (unilateral), industry (multilateral) or community protocol.

- Tokens in many forms have been in existence in business markets for many years and are growing in type and sophistication.

- Ordinarily, the token itself has no value. However, blurring of the lines between its role as a representation of value and its value in representation (becoming an asset) is driving not only innovation and investments in tokenization, but also the complexity of token approaches.

Tokens are digital assets, issued by the project, but can only be used as a method of payment inside project’s ecosystem, performing similar functions with coins, but the main difference between a blockchain-based cryptocurrency-coin and a token is that it also gives the holder a right to participate in the network; it may perform the functions of a digital asset, represent a company’s share, give access to the project’s functional and many more — with the launching of new projects unknown facets of tokens’ functional are discovered (What Is the Difference Between Coins and Tokens?). A ticket to a movie, for example, is a “real-life token” — you may use it at a certain time, at a certain place: you can’t go to the restaurant and pay your bill with a movie-ticket — a movie-ticket has its value only at movie-theatre (What Is the Difference Between Coins and Tokens?). Digital tokens function like movie-tickets — they have a certain use case only inside a certain project; however, creating a token is easier than creating an entirely new blockchain-based cryptocurrency coin, as you don’t have to instantiate new code or modify already existing one — only a standard template from platforms like Ethereum is required, that are blockchain-based and allow anyone to create tokens in just few steps (What Is the Difference Between Coins and Tokens?). Using a template for creating tokens provides smooth interoperability, so users can store different types of tokens in one wallet; Ethereum was the first to simplify the process of creating a token, being not the last reason why tokens flooded the market (What Is the Difference Between Coins and Tokens?). A Blockchain has the following key characteristics (Gupta, Manav):

- Consensus: For transactions to be valid, all participants must agree on its validity.

- Provenance: Participants know where the asset came from and how its ownership has changed over time.

- Immutability: No participant can tamper with a transaction after it’s been recorded to the ledger, if a transaction is in error, a new transaction must be used to reverse the error, and both transactions are then visible.

- Finality: A single, shared ledger provides one place to go to determine the ownership of an asset or the completion of a transaction.

The Linux Foundation is dedicated to building sustainable ecosystems around open source projects to accelerate technology development and industry adoption; founded in 2000, the Linux Foundation provides unparalleled support for open source communities through financial and intellectual resources, infrastructure, services, events, and training (The LINUX Foundation). The Linux Foundation and its projects form the most ambitious and successful investment in the creation of shared technology- it’s most recent, Hyperledger, an open-source community fostered to curate the development and advancement of blockchain technology rather than being relegated to a single platform like Ethereum, aiming to be more akin to the Apache Project as a cooperative of multiple projects dedicated to interoperable blockchain technology (The LINUX Foundation | Gupta, Manav). In spite of the aforementioned, as Ethereum already is what Hyperledger claims to represent, Ethereum does not authorize any entities with privilege to control decentralized applications derived from their open-source platform on an Open-Source or private Blockchain, or in essence, reinventing the best of the “blockchain” wheel for permissioned control by corporations or governments, claiming to fulfill four key elements (Gupta, Manav):

- Permissioned Network: collectively defined membership and access rights within your business network.

- Confidential Transactions: gives businesses the flexibility and security to make transactions visible to select parties with the correct encryption keys.

- Independence from Open-Source Cryptocurrencies like Ethereum: doesn’t require mining and expensive computations to assure transactions.

- Programmable: Leverages the embedded logic in smart contracts to automate business processes across your network

A permissioned-blockchain is not an open-source blockchain- in fact a permissioned blockchain is just another database- but that doesn’t necessarily preclude a use-case for an interoperable, Ethereum-based token with the ability to traverse between permissioned and open-source blockchains. Bitcoin is blockchain- and the most robust of its kind. The original concept of blocks and chains introduced by Satoshi Nakamoto (a name used by an unknown person or group of people) in 2008 only discusses blocks and chains in the context of a particular, concrete use case — namely a “peer-to-peer version of electronic cash.” Nakamoto was humble or, perhaps specifically, careful enough to not describe this as a new all-purpose technology, such as the currently accepted collective noun termed “blockchain,” (Kandaswamy, Rajesh, et al). The elegance in and breakthrough from Nakamoto’s work was to create blocks of records and chain them by combining older technologies into one architectural approach: using distributed communications networks (1964), digital signatures (1976), Merkle trees (1979), complementary currencies (4,000 Before Common Era [BCE])/digital currency (1983), proof of work (1993), Practical Byzantine Fault Tolerance (1999), and Secure Hash Algorithm (SHA)-256 (2001) ((Gartner: Blockchain Status 2018: Market Adoption Reality). Bitcoin is the most ambitious kind of blockchain: anyone can use Bitcoin’s cryptographic keys, anyone can run a full-node of the entire Bitcoin blockchain, and anyone can become a miner (the transaction validators) to service the network and seek a reward; miners can walk away from being a node, return if and when they feel like it, and get a full account of all network activity since they left at full profit/loss according to their network configurations (Bauerie, Nolan). Transaction data is permanently recorded in files called blocks; they can be thought of as the individual pages of a city recorder’s record book (where changes to title to real estate are recorded) or a stock transaction ledger (Block). Blocks are organized into a linear sequence over time (also known as the Blockchain); new transaction are constantly being processed by miners into new blocks which are added to the end of the chain (Block). As blocks are buried deeper and deeper, they become harder to remove (like upside pyramid) (Hyperledger Architecture, Volume 1). However, permissioned blockchains are much more exclusive for participation; for example, Ripple runs a permissioned blockchain: the startup determines who may act as transaction validator on their network, and it has included CGI, MIT and Microsoft as transaction validators, while also building its own nodes in different locations around the world, which means not everyone can join the Ripple network and validate Ripple transactions by mining for reward like Bitcoin or Ethereum; Hyperledger Burrow is a permissioned Ethereum smart-contract blockchain node that is capable of running Ethereum EVM smart contracts on a permissioned virtual machine (Bauerie, Nolan). The purpose of Burrow is to implement smart contracts (usually written in Solidity) in enterprise networks. Burrow is a node (client) that executes smart contracts on an authorized block chain compatible with the Ethereum Virtual Machine (EVM) (Regueiro, Mercedes). Hyperledger Burrow acts as a permissioned smart contract application engine whose primary job is executing and processing smart contract programs in a secure and efficient manner. It is built for a multi-chain environment that supports application specific optimization (Hyperledger Burrow). Some of the core capabilities of Burrow include transaction finality and high transaction throughput, in part, due to a Tendermint proof-of-stake consensus engine, while mitigating the marginal cost of securing a validator node is negligible, the reward scheme need not be inflationary as the transaction fees paid by users may be sufficient (Kwon, Jae). Recall that a Bitcoin blockchain transaction data is permanently recorded into files called blocks: they can be thought of as the individual pages of a bank-ledger or city recorder’s record book (e.g. stock from capital markets or real estate title)- like the Bitcoin blockchain blocks organized into a linear sequence over time, new transactions are constantly processed by open-source miners into new blocks which are added to the end of the chain; however, in a permissioned blockchain variant like Hyperledger Burrow, whereby tokenized assets (e.g. Ethereum-based ERC 20 and ERC721) may be ingested for interoperable transfer from a public blockchains on to a private blockchain for a given use-case, a limited number of miners or designated “validators” in a permissioned blockchain ecosystem participate in a consensus vote to approve or sign for blocks via: prevote, pre-commit and a commit- to receive more than 2/3 of commits means to receive commits from a 2/3 majority of validators (Kwon, Jae). A block is said to be committed by the network when a 2/3 majority of validators had signed and broadcast commits for that block; at each height of the blockchain a round-based protocol is run to determine the next block (Kwon, Jae). Each round is composed of three steps (Propose, Prevote, and Precommit), along with two special steps Commit and NewHeight: the Propose, Prevote, and Precommit steps each take one third of the total time allocated for that round- each round is longer than the previous round by a small fixed increment of time as this allows the network to eventually achieve consensus in a partially synchronous network; some uses cases require rapid network consensus systems and short block confirmation times before being added to the chain (Hyperledger | Kwon, Jae). Some of the core capabilities of Burrow include transaction finality and high transaction throughput, in part, due to a Tendermint proof-of-stake consensus engine for an improved developer experience that allows organizations to easily build blockchain applications for their business (Kwon, Jae). A consensus engine takes care of ordering and handling various transactions on the blockchain, and ensures high transaction output. It has a built-in set of transaction validators and also prevents any possible malicious attempts at hacking and forking the blockchain (Hyperledger Burrow).

The flexibility of Ethereum platform is what made it popular among the early Bitcoin and blockchain enthusiasts. In fact, while Bitcoin has been designed as a currency to transact value between different actors, Ethereum has been developed to extend the use of Bitcoin underlying technology and build a broader, general purpose blockchain; the Ethereum software layer has been built to allow the transaction of value in any shape or form, being it a currency, a house, an identity or the rights to produce a song, movie or any asset available utilizing a new programming language called Solidity, syntactically resembling JavaScript to express logic beyond the scope of transaction on the Bitcoin blockchain- for example, In example, a Smart Contract can implement the following logic: if both Mark and Bob send five Ether to Jack, then automatically send two Ether from Jack to Alice- Turing-complete, or more simply-stated, providing a computer (virtual-machine) with an executable set of instructions that is able to previously reference a previously existing set of instructions (or code-base) to properly arrange a execute a specified set of tasks to achieve an objective (D’Aliessi, Michele). Ethereum also allows anyone to create new digital currencies (or more specifically “tokens”) that can be exchanged by all Ethereum users. This enables a broad range of applications: from digitalizing the reward points at your favorite coffee shop, to creating whole new economies in specific markets (D’Aliessi, Michele). The purpose of Burrow is to implement Smart-Contracts (usually written in Solidity) in enterprise networks as a node (client) that executes smart contracts on an authorized blockchain compatible with the Ethereum Virtual Machine (EVM) (Regueiro, Mercedes). Burrow’s primary users are businesses aiming at value chain level optimization amongst other blockchain and smart contract benefits. These users require permissions on their blockchain deployments in order to fulfill numerous legal and/or commercial requirements for their applications designed to be a general-purpose smart contract machine and is not optimized for the requirements of any single industry (“Hyperledger Burrow.”). Only time will tell how and why permissioned blockchain technology may ultimately fail in the marketplace; for example, Burrow was designed as a general-purpose, cross-industry smart contract leveraging innovations from the Open-Source community as an ostensibly more secure product because it is a legally compliant, cryptocurrency-free, enterprise-grade product (“Hyperledger Burrow.”). Although some academics argue that business blockchain requirements vary as some users require rapid network consensus system and short block confirmation times before adding approved blocks to a given chain, other use-cases may compromise the aforementioned in exchange for lower levels of required trust- nevertheless, a permissioned blockchain will never be as secure because they are relegated by central points of failure, since all of their validation nodes, although “official” or sanctioned by a corporate entity, are actually few and far between and vulnerable by limitation in numbers, so they are more easily susceptible to concentrated hacks, like the recent Pigencoin compromise. Furthermore, Bitcoin-core developer Jimmy Song clarified the futility of permissioned or private blockchains from his personal experience engineering a private blockchain explaining (Song, J. (2018, June 11):

“Every single time I came back to the same thing, you have to have some central point of failure, in which case a blockchain makes zero sense […] I tried so hard […] to make that work, and I couldn’t find the way to do it without centralizing a large part of it, at which point it kind of becomes pointless.”

-Jimmy Song

Song further explains two major flaws with private blockchains frameworks like Hyperledger and Corda noting the “Oracle problem” and the “regulator problem;” the former becomes an issue when you bind a real-world asset to the blockchain noting “once you do that, then you lose a lot of of the protections that you get from say, the gold bar being in the vault; who does the gold bar belong to?” while the latter “regulator problem” refers to the regulatory entity reserving direct-access to a private federated chain determining the order of which transactions are added to the blockchain- like on the Hyperledger platform, specifically on Burrow, a modular blockchain client with a permissioned smart-contract interpreter partially developed to the specification of the Ethereum Virtual Machine (EVM) (“Hyperledger Burrow.” | Song, J. (2018, June 11). Permissioned blockchains may never succeed from a business perspective without a clear repeatable business model that is readily found in public blockchains because on permissioned, or private blockchains, there must be several technology components that ensure trust and security via reliable trusted-nodes (Litan, Avivah). Organizations must ensure that the entities running their validation nodes are reliable and trustworthy and unhindered from political and legal constraints; in public blockchains with cryptocurrencies, there are financial incentives for miners and node validators to not cheat the system but in private blockchains, there is not always a cryptocurrency attached to the network, eliminating that financial incentive (Litan, Avivah). Non-public blockchain governance must include the continual vetting of entities running the nodes to ensure they are trustworthy and reliable, which isn’t likely even if permissioned blockchains issue a token that can be used as an incentive for internal miners and validators, that token is limited in use to that blockchain unless it can be traded for more widely used crypto tokens- so a permissioned, or private blockchain is better off implemented as a sidechain or shard in a more common blockchain platform like Ethereum (Litan, Avivah). A trust-minimized environment depends on miner and validators that have the incentive to validate transactions in a scenarios that also minimizes the chance of a 51% attack; this requires decentralization and financial incentives for the miners (Litan, Avivah).

The question remains — what is the value proposition for blockchain in an enterprise context? Interoperability initiatives (such as Sawtooth Lake, Burrow, COCO, Plasma, Aion, Polkadot and Cosmos) between ledgers and between non-blockchain systems and those ledgers are immature; moreover, no common language exists for smart contracts across ledgers or industry contexts (Furlonger, David, and Rajesh Kandaswamy). User interfaces and convenient wallets for the masses are yet to be developed; software development toolkits are nascent- none of this gives CIOs comfort when trying to rebase their mission-critical priorities on a fragile/uncertain architecture and platform environment (Furlonger, David, and Rajesh Kandaswamy). Regardless of the implementation, one thing is a clear- blockchain is here to stay, so it would be absolutely reckless to forego due-diligence about how to integrate blockchain solutions for the enterprise. First, regardless of a private or public implementation, if a corporation doesn’t have a decentralized business model, a blockchain doesn’t make sense. There is no need for an undistributed ledger (or private blockchain), maintained in a corporate-cloud, separated from an open-source, distributed-ledger- a public blockchain enables people and entities that don’t know, and therefore don’t trust each other, to achieve transaction verification by transparently working together on an open-ledger because there is no longer a need to work with middle-men on an closed-ledger without smart-contracts.

A blockchain-based cryptocurrency would be a deterrent for bribes in the public sector, which amounts to roughly between $1.5 trillion and $2 trillion dollars annually, or 2 % of global GDP- and all it would take is adopting a cryptocurrency and using blockchain (Aldaz-Carroll, Enrique, and Eduardo Aldaz-Carroll). Merchants in the United States are losing approximately $190 billion a year to credit card fraud – much of it online, according to a 2009 LexisNexis study – while banks lose $11 billion dollars and customers loses about $4.8 billion dollars annually, so merchants lose almost twenty times as much as banks (Shaughnessy, Haydn). According to the Economist, the estimated total of healthcare fraud in 2011 was $272 billion dollars- or approximately 10% of total healthcare spending in America, or i/a/o $2.7 trillion dollars (17% of GDP), which would be the fifth largest country in the world by GDP (The $272 Billion Swindle). The World Health Organization estimates counterfeit pharmaceuticals cost cost over $200 billion dollars in lost revenue in 2017 and lead to more than 1 million deaths every year and can cause severe reactions (Finan, Terence). Transactions validated on an open-source, cryptocurrency ledger could potentially prevent a total estimated $2.68 trillion in fraud committed per year in the global public-sector, world-wide pharmaceutical industry, US healthcare and banking systems.

A 2016 report from the U.S. Department of Health and Human Services revealed that $10,345 is spent per person on health care; the cost of medication contributes to these rising healthcare costs; prescription drugs accounted for nearly 17 percent of all U.S. healthcare spending, while prices of prescription drugs also rose 10 percent in 2015 (Liebkind, Joe). One reason for this is the rising cost of bringing drugs to market; pharmaceutical companies and drug manufacturers invest billions to develop new drugs (Liebkind, Joe). In addition, the process of getting medication to patients also entails costs at each step: complex and unsecure supply chains further complicate matters (Liebkind, Joe). Manufacturers have to spend on solutions to address these issues, and the costs are passed on to consumers (Hyperledger Burrow). With a rise in counterfeit pharmaceuticals accounting for over $200 billion dollars in lost revenue in 2017, pharmacists and patients alike need greater visibility into where a particular medicine comes from and how it’s been handled throughout its journey (Finan, Terence). The World Health Organization (WHO) estimates counterfeit pharmaceuticals lead to more than 1 million deaths annually and can cause severe adverse reactions; given the potential for falsified pharmaceuticals to enter the supply chain, it’s imperative pharmacists and patients gain transparency into where medicines originate and if they’ve been tampered with, replaced, modified, or stolen (Finan, Terence). Through its immutability, transparency, traceability, and inalterability, a blockchain solution can drive substantive improvements to the pharmaceutical supply chain; using blockchain technology to track a drug through its entire lifecycle provides all parties assurances of its safety and authenticity (Finan, Terence). At every stage of the process, barcodes or smart tags could be scanned and recorded onto a blockchain ledger system that, in turn, records and creates an audit trail of the medicine’s journey; sensors can also be incorporated into the supply chain, with temperature or humidity being recorded onto the ledger system (Finan, Terence). This is especially important for drugs requiring refrigerated storage, such as insulin or expensive, specially manufactured medicines (Finan,Terence).

The answer comes in the form of blockchain technology, a form of software that runs across multiple computers, and creates a tamper-proof, indelible record of transactions; establishing an immutable, chain of custody, or permanent record of certain events that happen between many parties for one asset- there’s no question that having a public blockchain would be valuable, solving a longtime problem for the pharmaceutical industry: how to stop a flow of stolen or counterfeit pills entering the supply chain and trickling down to patients causing 1 million deaths annually, according to the World Health Organization (Finan, Terence).

Recently, a group of companies announced the MediLedger Project, which is creating blockchain tools to manage pharmaceutical supply chains; the group, which includes drug giants Genentech and Pfizer, has already completed a successful pilot program to track medicines (Roberts, Jeff John). If the project meets its goals, everyone from drug makers to wholesalers to hospitals will be recording drug deliveries on a blockchain; what this means in practice is that, at each step of the distribution process, a network of computers will vouch for the provenance and authenticity of a drug shipment—making it harder for thieves to unload stolen medications, or for counterfeiters to introduce fake wares (Roberts, Jeff John). Through the use of blockchain, the pharmaceutical journey could become more secure, transparent, and streamlined.

A permissioned-blockchain is not an open-source blockchain- in fact, it’s just another database in the conventional sense because only a few selected nodes can validate or sanitize a permissioned blockchain, which becomes central-points of failure easily compromised by 51% attacks, or more plainly stated “consensus hacks”; but that doesn’t necessarily preclude a use-case for an interoperable, Ethereum-based token with the ability to traverse between permissioned and open-source blockchains. Acknowledging historical reluctance in industry adoption of open-source applications and tools, an open-source project blockchain project championed by an established product may prelude a dynamic-entry from an open-source environment into a corporate ecosystem: like the Linux Foundation is open-source initiative, Hyperledger, in cooperation via Burrow client on the Ethereum ERC20 protocol-standard.